Analyses & Studies • Members

Saving and Investing in the UK: Key Options to Consider

By Matthieu Rident and Mimi Corden-Lloyd, Evelyn Partners

Whether you’ve just moved to the UK or have lived here for many years, navigating the financial landscape can be complex. Below, we outline several options to help you save and invest effectively in the UK.

Please note that the investment vehicles listed below are not necessarily suitable for all individuals, and this does not constitute formal investment advice. As with all investments, the following investment options carry risk. The value of an investment, and the income from it, may go down as well as up and you may get back less than originally invested. Tax treatment depends on individual circumstances and is subject to change.

Individual Savings Account (ISA)

ISAs are one of the most popular savings vehicles in the UK. Their main appeal lies in tax efficiency, as investments held in ISAs are exempt from tax on returns and dividends. Adults can contribute up to £20,000 per tax year, allowing for long-term, tax-free growth.

There are several types of ISAs such as Cash ISAs and Stocks & Shares ISAs, all of which can be used for a variety of savings and investment needs.

It is also worth noting that Junior ISAs (JISAs) are available to children, with a reduced annual allowance of £9,000 a year until they turn 18.

Pensions

Pensions are another cornerstone of tax-efficient saving in the UK. Unlike in France, most UK pensions are capitalised, meaning your contributions are invested to grow over time.

Key features include:

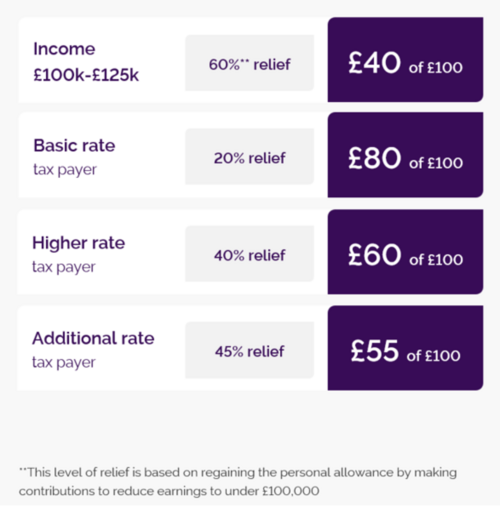

- Tax relief on contributions: Contributions up to the Annual Allowance are made from gross income, reducing your taxable income. The Annual Allowance is the total amount of contributions that can be paid into all pensions for an individual before a tax charge applies. Your Annual Allowance is up to £60,000 per year, or up to 100% of earnings, whichever is lower. This will potentially reduce to £10,000 if you have already accessed your pension or if your income is over £260,000.

- Tax-free growth: Investments within the pension grow free from income and capital gains tax.

- Tax on withdrawal: Income Tax is payable at your marginal rate when you begin drawing benefits, typically from age 55.

Business owners can make pension contributions through the company, which are typically corporation tax deductible, making them a powerful planning tool.

Tax relief on pension contributions – net salary in your pocket vs money in the pension

General investment account (GIA)

For savings beyond ISAs and pensions, a GIA offers flexibility to invest in a wide range of assets such as shares, bonds, funds, and alternatives. However, unlike ISAs and pensions, returns may be subject to:

- Income tax

- Dividend tax

- Capital gains tax

GIAs are typically simple to set up and can be useful for medium- to long-term investing, especially when ISA and pension allowances have been fully utilised.

Cash

While the above investment options focus on long-term growth, it’s also important to consider where to hold cash as a safer option for emergencies, short-term needs or planned purchases.

- Bank savings: Check interest rates regularly. Interest is liable to income tax after allowances (e.g. Personal Savings Allowance). It is worth bearing in mind that the FSCS protection scheme covers up to £85,000 per person, per institution if a bank fails.

Gilts

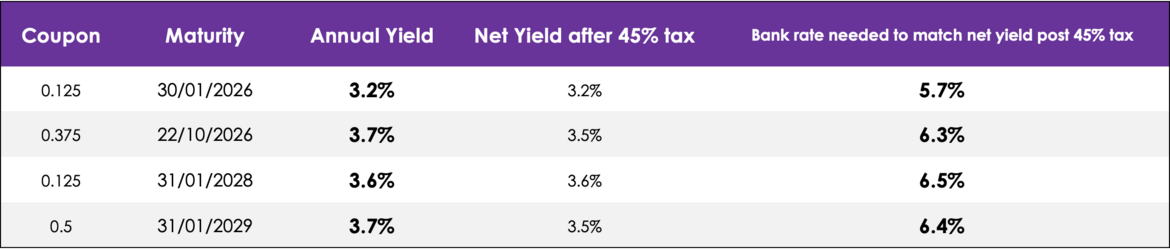

An alternative to cash for individuals is the purchase of Gilts, which are bonds issued by the UK Government. Buying short-dated Gilts with low coupons can be an attractive tax-efficient cash alternative. This is mainly because only the small coupon attracts income tax at the individual’s marginal rate (if it is outside your Personal Savings Allowance), whilst no tax is payable on the capital gain element of the Gilt. The below table illustrates the tax advantage with an example of an additional rate taxpayer.

All figures as at 20th October 2025. Current or past yield figures provided should not be considered a reliable indicator of future performance

Source: Evelyn Partners/Refinitiv

Gilts are very liquid and can be bought and sold easily (even before their maturity), which could make them a good alternative for short-term cash.

For businesses, it is worth bearing in mind that the tax exemption does not apply, as all gains are taxed at corporation tax rates. However, T Bills (ultra short bonds) may offer an attractive rate for business cash.

Specialist planning

For more complex needs, additional structures may be appropriate, however advice should be taken before investing in these as they are not suitable for everyone:

- Trusts – for estate planning and asset protection

- Venture Capital Trusts (VCTs) – for high-risk, tax-efficient investing

- Offshore Bonds – for deferring tax and managing income streams

If you have any questions about your personal money or your business’ finances, we would be delighted to discuss these in more detail with you.

UK wealth manager, providing financial and investment advice.